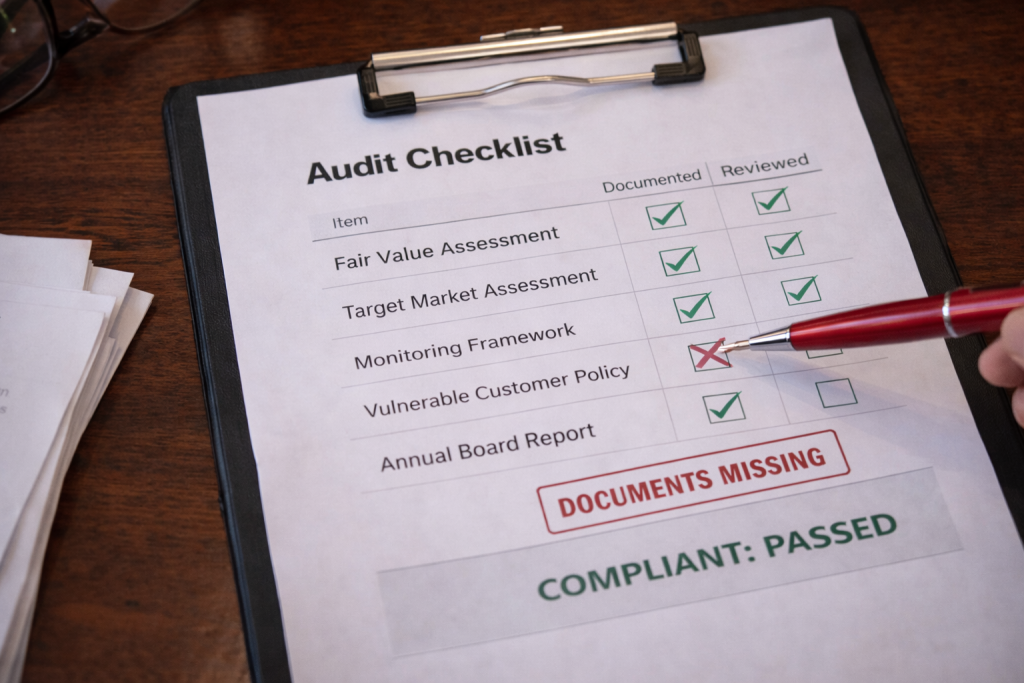

The written evidence the FCA expects to find at any IFA firm on examination. Produced by someone with the professional background to do it properly, not just the willingness to try.

Consumer Duty does not ask firms to try to deliver good outcomes. It requires them to prove they have. The FCA’s position on this is clear: if the documentary evidence does not exist, the good outcome is treated as not having been achieved.

For IFA firms, this means maintaining a documented evidence base across seven areas and being in a position to produce it on request. Most firms understand what is required in principle. Rather fewer have actually got the paperwork in order.

The Consumer Duty Documentation Guide sets out, in plain English, exactly what the FCA expects to find on examination at any IFA firm. It includes a 15-item checklist and a good practice comparison drawn from FCA thematic review findings, set alongside the most common gaps. Download it, work through the checklist, and you will have a clear picture of where the gaps are before you book a call.

FCA FINDING : Good outcome: Achieved

FCA FINDING : Good outcome: Not Achieved

If the documentary evidence does not exist, the good outcome is treated as not having been achieved.

The written evidence base the FCA expects to find at any IFA firm on examination.

A detailed analysis of your charges relative to benefits delivered across your entire client base. Covers all client segments including vulnerable clients, identifies cross-subsidies, and presents methodoly in board-ready form.

This is the document that attracts the closes FCA scrutiny, and where the Cost Lawyer background is most directly relevant.

£1,500 – £2,500

A written TMA for each product or service on your panel, covering the postivie target market and – just as importantly – the negative target market.

A regulatory document under product governance rules. Not to be confused with marketing materials. ONe assessment per product or service.

£500 – £900

The writtent framework specifiying what your firm measures across the four consumer outcome areas, how it is measuered, and how often.

This is not data analysis. It is the documented structure that directs your evidence-gathering and gives the FCA reason to believe your monitoring is systematic.

£800 – £1,400

A written policy covering how your firm identifies vulnerability, what triggers an adapted response, and how you monitor outcomes for vulnerable clients as a distinct group.

Require under FG21/1. Most small practices are working from something drafted quickly and never properly reviewed.

£400 – £700

Ghost-writing the annual board-level outcomes review that every firm is required to produce and retain. Draws together your MI data and outcomes evidence into a document that demonstrates genuine board engagement.

Recurring annual work. The document most principals find hardest to produce alone.T

From £1,200 p.a.

All fees indicative. Exact scope and final fee agreed in writing before work begins. | Delivered for your compliance review and approval. | Compliance sign-off not included.

Most financial copywriters approach regulatory documents as writing assignments. They read the FCA’s guidance, work out what is required, and produce something that reflects the specification. For most regulatory documents, that is a reasonable description of the process.

Fair Value Assessment is different, and the distinction is worth understanding.

My training as a Cost Lawyer was built around the professional analysis of whether charges were fair and reasonable relative to the work performed and the value delivered. That is not merely similar to what a Fair Value Assessment requires. It is the same analysis, conducted to the same standard of rigour, carried out in a different regulatory context. I have spent a career doing this kind of work. When I produce a Fair Value Assessment for an IFA firm, the analytical discipline behind it comes from professional training, not from reading the FCA’s guidance notes the week before.

No financial copywriter I am aware of can say the same. If that matters to you, and given what the FCA tends to do with inadequate Fair Value Assessments it probably should, it is worth having a conversation.

A call is arranged. You walk me through your firm's charging structure, client base and existing documentation. I ask specific questions about your services and the evidence you already have in place.

I produce the document. Research, drafting, regulatory cross-referencing. You do not need to supply source material beyond what comes out of the briefing conversation.

You review it. Your compliance function signs off. If there are questions, I am happy to address them directly.

You have a defensible document. One that the FCA can examine, the board can own, and that gives a proper answer to the question: how does your firm actually know it is delivering good outcomes?

Consumer Duty documenation produced to the standard the FCA actually expects to find.

STEP ONE

2 TO 4 WEEKS

AT YOUR PACE

STEP ONE

You walk me through your firm's charging structure, client base and existing documentation. I ask specifi questions: 20 to 30 minutes is usually enough to agree scope and brief

2 TO 4 WEEKS

Research, drafting, regulatory cross-reference. You do not need to supply source material. Everythingn happens on my side

AT YOUR OWN PACE

Your compliance team reviews the document. If there are questions, I address them directly. One revision round included.

The FCA can examine it. The board can own it. It answers the question: how does your firm know it is delivering good outcomes?

No complicated onboarding. | No source material required from you. | Fixed fee agreed before any work begins.